Rate Hikes and Cuts Explained — Why Markets Act Opposite

The central bank just cut rates. The currency went up. This is not a reporting error or a market glitch. It is one of the most repeatable patterns in prop trading, and it happens precisely because almost every rate hikes and cuts explainer stops at the most surface-level version of how central bank decisions move currency markets. The standard version says: rate hike — currency strengthens, rate cut — currency weakens. That is true for long-term directional trends. It is routinely wrong for individual rate decisions, and trading it as a binary rule gets you wrong-footed on exactly the days that produce the largest forex moves.

What determines whether a rate hikes and cuts decision strengthens or weakens a currency is not the decision itself. It is the gap between what the central bank delivered and what the market had already priced in before the announcement arrived. That distinction is what rate hikes and cuts explained at the trading level actually means, and it is the framework that keeps you from being blindsided by reactions that look backwards on the surface.

Rate hikes and cuts explained: central banks raise rates to slow inflation and attract capital inflows, which strengthens the currency; they cut rates to stimulate growth, which weakens it. But markets price these decisions ahead of time through interest rate futures and swap markets. When a cut is smaller than the market expected, the currency can strengthen — because relative to what was priced in, the decision is less bearish than anticipated.

What Rate Hikes and Cuts Do to a Currency

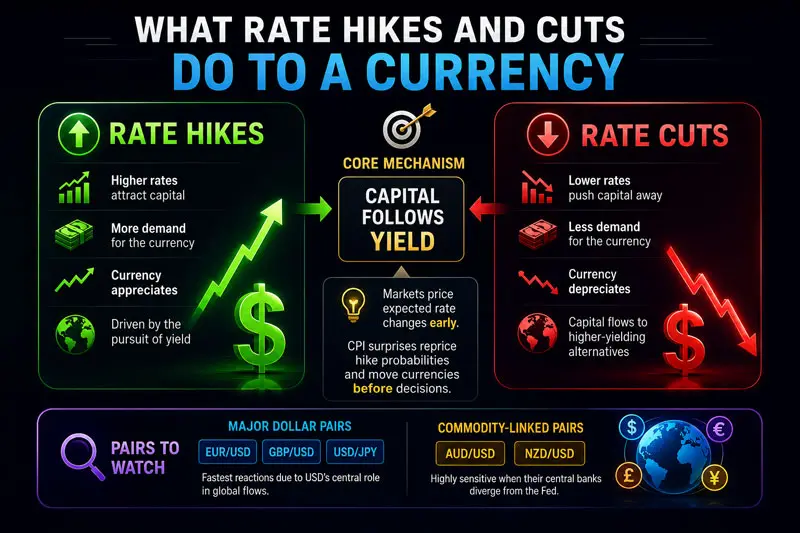

Rate hikes and cuts move currencies through a single foundational mechanism: capital follows yield. When a central bank raises its benchmark interest rate, deposits, government bonds, and short-term money market instruments denominated in that currency offer higher returns. Global capital — pension funds, insurers, sovereign wealth funds — reallocates toward those higher yields. Demand for the currency rises, and it appreciates.

A rate cut runs the same logic in reverse. Lower rates reduce the return on that currency’s assets relative to alternatives elsewhere. Capital flows toward better-yielding options. Demand for the currency falls, and it weakens over time. This mechanism is real and it drives major long-term trends in EUR/USD, GBP/USD, and the dollar crosses.

The problem is treating it as a trading rule for announcements. By the time the rate hikes and cuts decision prints, the capital realignment implied by that decision has already started — sometimes weeks earlier — because markets price expected rate changes as soon as the probability shifts, not when the vote is official.

CPI news is the clearest example of this in practice. Central banks set policy around inflation, so when CPI prints above forecast, markets immediately reprice the probability of a rate hike — and the currency rallies before any actual rate hikes and cuts decision has been made. The announcement that eventually follows either confirms or deviates from what price already built in.

Which pairs to watch matters too. The best forex currency pairs for trading rate decisions are the major dollar pairs — EUR/USD, GBP/USD, USD/JPY — because the US dollar sits at the centre of global capital flows and rate differential moves transmit fastest through those markets. Commodity-linked pairs like AUD/USD and NZD/USD are highly sensitive to rate changes when their central banks diverge from the Fed.

Rate Differentials — The Number That Actually Moves Price

Rate differentials are what forex markets actually price — not a single central bank’s rate in isolation.

EUR/USD moves on the spread between the European Central Bank rate and the Federal Reserve rate. If the Fed hikes 25 basis points while the ECB hikes 50 basis points over the same period, EUR/USD can rise even though US rates went higher in absolute terms. The euro became more expensive faster. The dollar strengthened, but the euro strengthened more. The pair’s price reflects that differential — not either rate on its own.

This spread is also the foundation of the carry trade: borrow in a low-rate currency, invest in a higher-yielding one, and earn the differential while holding. Historically the Japanese yen and Swiss franc have been the primary funding currencies, while the Australian and New Zealand dollars have served as common receiver currencies. Leverage in forex amplifies the yield spread — which makes carry positions attractive in stable rate environments and extremely dangerous when the differential compresses sharply or reverses.

Covered interest rate parity says forward exchange rates should theoretically offset any yield advantage, making carry trades unprofitable in theory. In practice, uncovered carry works because capital allocation is slow, global flows are sticky, and markets are not perfectly efficient. But when rate hikes and cuts expectations shift sharply — a central bank signals a pivot, a funding currency raises rates unexpectedly — that stickiness snaps, and the unwind is fast and disorderly.

If you want to get a funded account and trade macro events effectively, the rate differential framework is the foundation. Every carry position, every pair selection, every entry timing decision around central bank events derives from understanding where two central banks sit in their respective rate cycles relative to each other — not where either one sits in isolation.

Why a Rate Cut Can Strengthen a Currency — The Priced-In Mechanism

This is the mechanism that produces the “wrong” currency reaction most often, and it is almost never explained correctly.

Markets price rate hikes and cuts decisions before they happen. Interest rate futures contracts, overnight indexed swaps, and options markets all assign probabilities to possible outcomes weeks in advance. When those markets show a 90% probability of a 50 basis point rate cut, that cut is effectively already priced. The currency weakened when the probability climbed to 90% — not when the committee voted. By the time the official announcement arrives, the price has already moved.

The useful mental model here: a rate hikes and cuts decision is like a test. The market takes a guess at the score beforehand. The currency moves based on whether the actual score was higher or lower than the guessed score — not on whether the score itself is high or low. This one framing change explains the majority of “counterintuitive” rate reactions you will see.

When markets price in a 75 basis point rate cut and the central bank delivers 25 basis points, the currency strengthens sharply. Not because a rate cut is bullish — it is not — but because 25bps is dramatically less dovish than the 75bps that was priced. Relative to the market’s expectations, the central bank just tightened. Holders of that currency are now earning a better yield than they thought they would be getting. They buy. The currency rallies.

The inverse is equally important. When markets price a 25 basis point rate hike and the central bank delivers 50 basis points, even though rates just rose meaningfully, the currency can still fall if the statement language suggests the hiking cycle is now close to peaking. The bigger-than-expected hike is interpreted as pulling forward future hikes, not adding to them.

This is why the only question that matters before a rate hikes and cuts decision is not “will they hike or cut?” It is: “what is currently priced, and how does today’s decision compare to that?” How to trade forex news at the decision level is fundamentally a consensus-versus-outcome trade. The consensus is not what you read in the financial press — it is what interest rate futures are pricing in the 48 hours before the announcement.

How Forward Guidance Shapes rate hikes and cuts Decisions Before the Announcement

By the time a rate hikes and cuts decision prints, most of the informed positioning has already happened.

Central banks do not like to surprise markets — they prefer orderly repricing. They signal shifts weeks in advance through the minutes of prior meetings, through speeches by individual committee members, and through careful language changes in public statements. The US Federal Reserve’s dot plot — a chart showing where each committee member expects rates to be over the following three years — is published four times a year and frequently moves currency markets more than the actual rate vote that accompanies it. When the dots shift downward toward more cuts, the dollar sells off. When they hold higher-for-longer than expected, it rallies.

Pre-meeting economic data does most of the rate-expectation shifting between decisions. Above-forecast CPI readings push rate futures toward fewer cuts and tighter policy. Weak employment figures push them toward more easing. Each release is a new input into the market’s running probability model, and the currency moves incrementally with each one. By decision day, the market has typically converged on a strong consensus.

This is where the pre-decision trade lives. Fibonacci retracement levels become highly relevant after major rate hikes and cuts expectation shifts — the sustained trends created by hawkish or dovish pivots tend to retrace into identifiable levels before continuing, giving structured entries on a directional view built on fundamentals. Support and resistance zones formed during the expectation repricing phase tend to hold on subsequent tests because the same fundamental logic that created the initial trend reinforces those price levels.

The most actionable rate hike and rate cut trades play out over days and weeks before the decision — not in the seconds after the print.

Rate Hike Forex Reactions — Reading Price After the Announcement

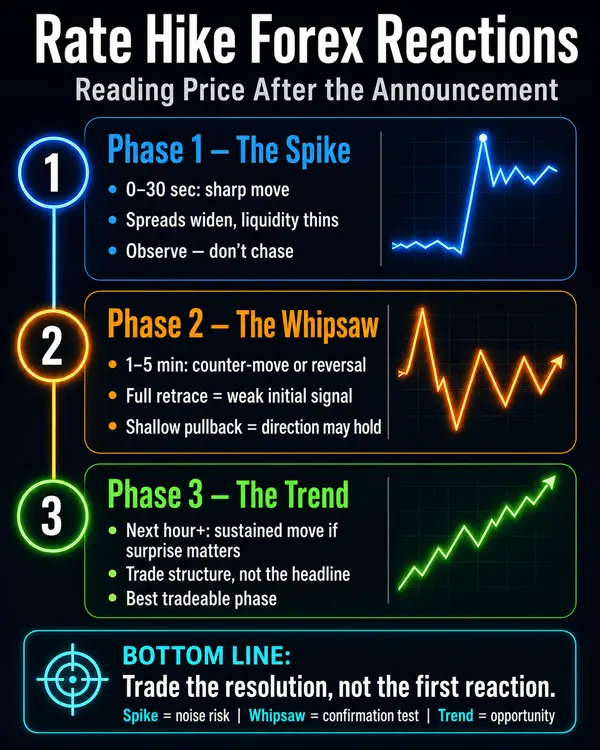

rate hikes and cuts announcements produce three distinct price phases. Knowing which phase you are watching determines whether you have a trade or noise.

Phase one — the spike. The moment the number prints, price moves sharply. Thirty to 100 pips in the first thirty seconds is common on major rate hikes and cuts decisions. Spreads widen sharply as liquidity thins at the exact moment of release. Market orders fill at meaningfully worse prices than displayed. This is the phase to observe, not to trade — execution is unreliable, and the initial direction reverses frequently.

Phase two — the whipsaw. Within the first one to five minutes, a counter-move develops. Algorithmic systems, short-term speculators, and stop-run mechanics create a partial or full reversal of the initial spike. If you entered during Phase 1, this phase typically kills the position. If you waited, the whipsaw tells you whether the initial move had conviction: a full retracement of the spike suggests the initial direction was stop-driven and uninformative; a shallow pullback that holds structure suggests the market is accepting the initial direction as correct.

Phase three — the trend. If the decision meaningfully deviated from what was priced in, a sustained directional move develops over the following hour and often extends into the next session. This is the tradeable phase. The direction is visible from Phase 1 and 2’s resolution. The entry is defined by structure, not by a bet on the headline.

One addition that traders underestimate: the post-decision press conference frequently matters more than the vote itself. Central bank governors speak for 45 to 60 minutes after the print, and language around the future path of rate hikes and cuts — the pace of the next move, whether cuts are conditional on data, dissenting committee views — can fully reverse the initial reaction or extend it significantly.

After the whipsaw phase resolves, watch for BOS and CHoCH on the 15-minute or 1-hour chart. A clean structural break following the Phase 2 noise, at a sensible higher-timeframe level, is the higher-probability entry. It costs you some of the Phase 3 move to wait for it — that is the price of executing at a real level rather than chasing the spike. Trading rate hikes and cuts announcements through a prop firm account makes that discipline non-negotiable, because a poorly-timed Phase 1 entry can consume a significant portion of a daily drawdown limit before the trade has any chance to develop.

The rate hikes and cuts Impact on Carry Trades

When a high-yield central bank cuts rates, carry trades face the most concentrated pressure in the entire forex market.

Carry trades are structurally simple: long the higher-rate currency, short the lower-rate currency, earning the yield spread daily. As long as the rate differential holds and the higher-yield currency stays stable, the trade compounds quietly. The structural problem is the exit. Carry positions are typically large, levered, and concentrated in the same institutional hands. When the high-rate central bank cuts — compressing the yield advantage that justified the position — those participants unwind simultaneously. AUD/JPY, NZD/JPY, and EUR/JPY can fall sharply and fast because the exit is coordinated by the same fundamental shift that originally created the trade.

The force multiplier is that carry positions are often sized aggressively because the strategy is marketed as low-volatility income. During stable periods, the daily yield accrual disguises the latent directional risk. When the rate cut impact hits and the differential collapses, that sizing becomes a liability — everyone is selling the same pair at once, gaps through stop-loss levels are common, and the reversal happens faster than most participants can adjust.

PropLynq traders active on yen cross pairs should be particularly aware that carry unwinds are not gradual. When a central bank that maintained ultra-low rates begins normalizing — as the Bank of Japan did during its policy normalization period — carry positions built over months can reverse in days. The pip velocity during carry unwinds is comparable to high-impact news events, not ordinary session volatility.

A forex lot size calculator is not optional in carry-sensitive environments. Position size that is manageable during a stable rate differential can become impossible to hold — from both a risk and margin perspective — during a fast unwind. Reducing size when rate cycle uncertainty is elevated is not timidity; it is the adjustment that lets you survive the volatility and remain positioned to re-enter at better levels.

Positioning Around rate hikes and cuts Decisions Without Blowing Risk

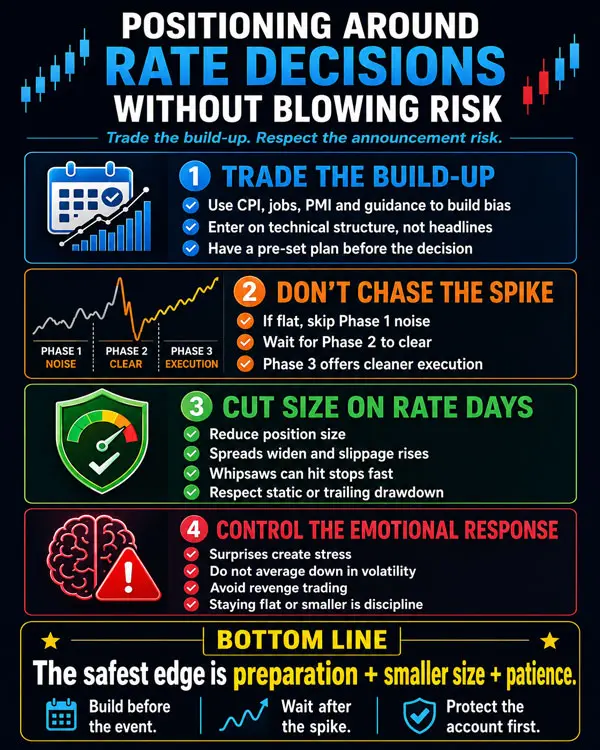

The most consistent approach to rate hikes and cuts events is to trade the build-up, not the announcement itself.

Pre-meeting data — CPI, employment reports, retail sales, PMIs — and forward guidance language create directional biases before the vote. When inflation has consistently printed above forecast and central bank language has shifted toward more hawkish phrasing, the currency is probably building an upside bias. Build the position when technical structure gives you an entry: a retracement into a prior level, a continuation of the trend after a pullback, a consolidation breakout aligned with the directional bias. Hold into the decision with a pre-set plan for how you handle both outcomes.

If you are flat at announcement time, do not chase the spike. The market always produces a setup after the Phase 2 noise clears. What it almost never produces is a clean entry during Phase 1 or in the first few minutes of the reversal. The cost of waiting for Phase 3 is a smaller piece of the move — which is a reasonable price to pay for genuine execution.

On rate decision days specifically, reduce your position size regardless of conviction level. Spreads are wider, slippage adds hidden cost, and even the correct directional call gets stopped by Phase 2 whipsaws if the position is sized as if it is a normal session. Understanding static vs trailing drawdown in your account rules matters here in a practical way — a Phase 2 whipsaw on an oversize position might breach your daily drawdown limit before Phase 3 ever has a chance to develop, even if the longer-term direction of your original trade was correct.

Surprise outcomes are also an emotional stress test. When the market moves hard against a pre-decision position on an unexpected outcome, the impulse is to add to the trade to recover quickly. Revenge trading after a loss on a rate decision day is one of the most common ways funded evaluation accounts get breached — not because the original view was wrong, but because the emotional response doubled the size into a volatile environment. Staying flat or reducing after a surprise is not a failure of conviction. It is the correct response to an environment where information has changed.

Rate Decisions and Prop Challenges — The Drawdown Problem

Inside a funded evaluation, rate decisions create one specific structural risk: the speed of the adverse move, not just its direction.

PropLynq’s Two-Step challenge carries a 5% daily drawdown limit and a 10% maximum drawdown. On a $100,000 account, the daily floor is $5,000. A 100-pip adverse spike on EUR/USD at 0.5 lots — a position size that is entirely reasonable for controlled risk-taking on a normal session — costs exactly $5,000. That single release has consumed the full daily limit. One hundred pips on an FOMC, ECB, or Bank of England decision day is not an exceptional move. It is within normal bounds.

The framework for funded traders around rate decisions is straightforward. Before the announcement, calculate the worst-case pip move the release could reasonably produce based on the pair’s volatility history around similar events. Size your position so that worst case represents no more than 25 to 30 percent of your daily limit — roughly $1,250 on a $100k Two-Step account. Set a pre-decision rule about whether you hold through the print or close beforehand. Either choice is valid; what is not valid is making that decision during the announcement itself, when emotion and price movement are both running against clear thinking.

How to pass a prop firm challenge through a rate-decision-heavy period ultimately comes down to surviving these events at reduced exposure — not calling them correctly. A trader who exits flat before every major rate decision and re-enters after Phase 3 structure forms will consistently outperform the trader who holds through every print at full size, because the wrong-direction surprises at full size cost more than the correct predictions gain.

Rate Hikes and Cuts Explained: The Takeaway

Rate hikes and cuts are not binary signals. They are events measured against a moving target — market expectations — and the direction of price is determined by whether the outcome landed above or below that target, not by which way rates moved.

The central bank that cuts rates but cuts less than the market expected has not weakened its currency at that moment. It has, relative to the consensus, tightened it. That counterintuitive reaction is not an anomaly. It is the market correctly processing information — the same market that had already moved to price the larger cut that never arrived.

This is what rate hikes and cuts explained at the level that actually matters for trading means: know what is priced before you read the number. Form your directional view from the pre-meeting data and forward guidance shifts. Build positions in the build-up phase, where the risk-reward is cleaner and execution is reliable. Reduce size on decision day. Wait for Phase 3 to enter if you are not already positioned. And never add to a losing position in the minutes following a rate surprise — that is where evaluation accounts end, not where they are recovered.

Miles Rowan Keene

As Senior Market Strategist at PropLynq, I write about market structure, trading psychology, and risk-first execution. My focus is on turning complex market behavior into clear, actionable lessons for both developing and experienced traders. I specialize in educational content covering funded account rules, drawdown management, trade planning, and strategy refinement, with the goal of helping traders build consistency through discipline, preparation, and a deeper understanding of how professional trading environments operate.

Weekly Trading Insights

Market analysis and trading tips delivered every Monday. No spam, unsubscribe anytime.

Comments

All comments are reviewed before publication · Text only · No links

No comments yet — be the first.