Revenge Trading After a Loss – How It Breaks Evaluation Accounts

Let me a paint you a picture befor going deep in revenge trading after a loss.You’re down 1.3% on the session. The setup was valid. The stop got hunted by a wick — you’ve seen it a hundred times — and it caught you. You know what this market is doing. You know where it’s going next.

You open another position.

Not because you’re angry. Because you see it.

That’s the version of the story most traders tell themselves. And that exact framing — calm, analytical, certain — is what makes revenge trading so hard to catch from the inside, and so reliable at breaking evaluation accounts.

Revenge trading is not the version where you’re slamming a desk or doubling your size in a moment of obvious fury. Most of the time it’s quieter than that. It feels like clarity. It feels like reading the market correctly after a mistake. The trader who’s in the middle of a revenge trading sequence rarely thinks they are — they think they’re trading. By the time the behaviour is undeniable, the daily drawdown limit is gone and so is the challenge.

The Trade That Feels Completely Justified (But Isn’t)

The internal monologue during a revenge trade is specific and recognisable once you know what to listen for. It sounds something like this:

- “This is a different setup.”

- “I understand exactly why the first trade failed — that won’t happen again.”

- “If I size slightly larger I can recover this in one clean move.”

- “This is the actual direction.”

None of that sounds like anger. All of it sounds like analysis. That’s the problem.

What actually happened is this: the losing trade generated an emotional signal — frustration, urgency, the specific discomfort of being wrong on a setup that felt clear. That signal warped the decision-making process before you noticed. The new trade isn’t built on a clean read of the market. It’s built on a clean-sounding narrative your brain constructed to justify what the emotional state was already pushing you toward.

Psychologists call this post-hoc rationalisation: the decision comes first, the reasoning follows. Because the reasoning feels genuine — because you actually believe the setup is valid — no internal alarm fires. You’re not overriding good judgment. In the moment, you feel like you are the good judgment. The trade that blows the challenge feels exactly like the trades that don’t.

This is the structural problem with revenge trading that most writing on the subject misses entirely. It gets treated as an impulse control problem — as if the fix is slowing down, breathing, being more disciplined. But you can’t apply discipline to a state you don’t know you’re in.

What Revenge Trading Actually Feels Like From the Inside

For an advanced trader, the useful question isn’t what revenge trading is — it’s what it feels like in the moment, specifically, so it can be caught in real time. The experience has four consistent components.

The conviction spike. After a losing trade, a meaningful subset of traders don’t experience doubt — they experience heightened certainty. The loss “clarified” something. The next read feels sharper. This is almost always a red flag, not because losses can’t teach you anything, but because a genuine edge doesn’t get stronger because you had a bad trade. What got stronger was the emotional need to be right, wearing the costume of a sharper thesis.

The urgency that feels like focus. Revenge trading moves fast. Not because the next setup is obvious — because the emotional state creates a sense of time pressure. You need to be in the market now, while the session is still recoverable, while the move is still live. That urgency is not market information. It is anxiety in the language of opportunity. The critical tell: genuine setups wait for their conditions. Revenge trades find their conditions immediately after the loss.

The size rationalisation. Position sizing is the tell that doesn’t lie. Revenge trades are frequently larger than the plan calls for, and the reasoning is always coherent: “I’m more confident in this one.” “The stop is tighter so I’m actually risking less.” “I need to recover before the session closes.” These are not risk management arguments. They are emotional states translated into the syntax of risk management. When leverage is in play, those inflated sizes compound the drawdown damage faster than most traders anticipate — the interaction between position size and leverage is covered in detail in our guide to using leverage in forex and crypto.

The truncated pre-trade process. Before the revenge trade, did you complete your standard pre-trade checklist? Most traders who are revenge trading did not — or ran through it so quickly it was theater. The urgency state and a rigorous process are structurally incompatible. If you notice the checklist got abbreviated or skipped, that’s the signal. Not conclusive proof — but a diagnostic signal worth taking seriously.

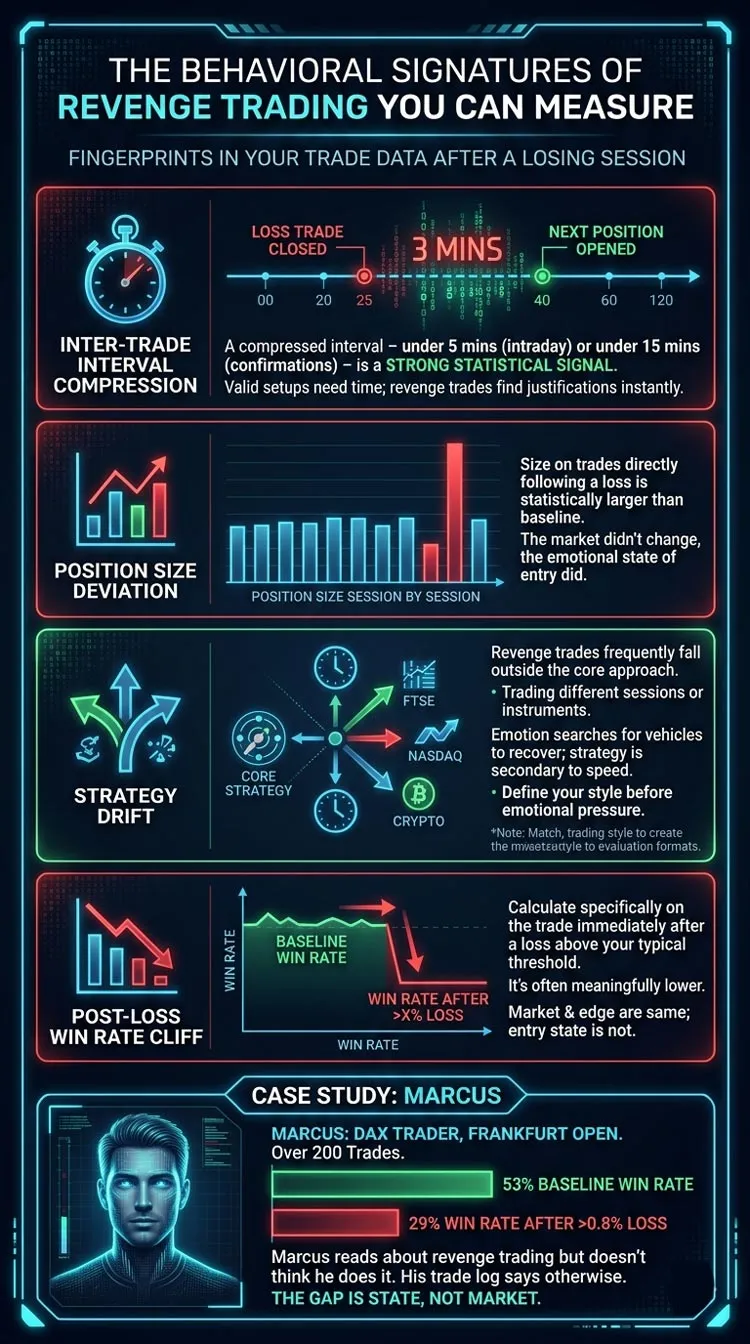

The Behavioral Signatures of Revenge Trading You Can Measure

Revenge trading leaves fingerprints in trade data. After any losing session, pull your trade log and look for these four patterns before you start analysing why the trades themselves were wrong.

Inter-trade interval compression. How much time elapsed between the losing trade closing and the next position opening? A compressed interval — under five minutes for most intraday strategies, under fifteen for setups requiring confirmation — is a strong statistical signal. Valid setups require time to develop. Revenge trades don’t wait; they locate a justification immediately after the loss.

Position size deviation from your baseline. Plot your sizes session by session. Revenge trading shows up as spikes: the size on trades directly following a loss is statistically larger than your average. The market didn’t change. The edge didn’t change. The emotional calibration of the entry did.

Strategy drift. Revenge trades frequently fall outside the trader’s core approach. Traders who specialise in one session trade a different one. Traders who work one instrument suddenly add another. The justification sounds strategic. The pattern is diagnostic: the emotional state is searching for any vehicle to recover the loss, and strategy becomes secondary to speed. This is precisely why matching your trading style to the evaluation format before starting a challenge matters — traders who have a clearly defined approach before emotional pressure arrives are significantly harder to drift off it.

Post-loss win rate cliff. Calculate your win rate specifically on the trade immediately following a losing trade above your typical threshold. For most traders, this number is meaningfully lower than their baseline. The market is the same. The edge is the same. The entry state is not.

Consider Marcus — a hypothetical but realistic example. Marcus trades the DAX during the Frankfurt open. Over 200 trades, his baseline win rate is 53%. On the trade immediately following any loss greater than 0.8%, his win rate is 29%. Marcus has read about revenge trading. He’d tell you he doesn’t do it. His trade log says otherwise. The gap between 53% and 29% is not the market. It’s the state.

Why Prop Firm Evaluations Are Built to Expose It

Evaluation accounts don’t cause revenge trading. But they create conditions where its consequences are immediate and irreversible in ways that personal trading accounts are not.

In personal trading, a bad day is expensive. In an evaluation, a bad day can be the last day. That structural difference — a hard ceiling on daily losses — is not a minor procedural detail. It fundamentally changes the psychological stakes of every losing trade and creates exactly the conditions under which revenge trading becomes most destructive: urgency, a visible limit being consumed, and no existing profit buffer to absorb it.

The mechanism is direct: most prop trading evaluation frameworks enforce a daily drawdown limit alongside a maximum account drawdown. Hit either one and the challenge ends — no recovery, no continuation. This means that a revenge trading sequence doesn’t just cost money. It triggers a hard stop that eliminates the ability to continue. The very impulse to recover is the one that closes the account.

There is a second amplifying effect: most traders begin evaluation accounts with no cushion of existing profit. A loss on day three is psychologically different from a loss on day thirty when you’re sitting 4% in profit. Early-session losses, with no buffer and a visible daily ceiling already partially consumed, produce the worst possible conditions for revenge trading: the account feels like it needs to be recovered now, and the daily limit feels like it’s closing in. The exact pressure profile also varies by format — the difference between 1-step and 2-step prop firm challenges changes how much runway exists before a revenge trading session becomes unrecoverable.

This is the structural trap. And revenge trading is what walks into it.

How One Bad Session Compounds Into a Failed Challenge

The abstraction of “revenge trading breaks evaluation accounts” doesn’t communicate how fast the sequence actually unfolds. Here is the mechanical version.

A trader is running a $100,000 evaluation. PropLynq, for example, structures its challenges with a maximum drawdown limit alongside a daily loss limit that functions as an earlier tripwire — designed to prevent a single session from consuming a disproportionate share of the account before the trader has a chance to reset. On a $100,000 account, these limits translate to hard ceilings the trader must stay inside within each session and across the account’s lifetime.

The trader loses 1.8% in the morning session on a legitimate setup. That is $1,800. Room remains. The session is technically recoverable.

Revenge trade one: slightly larger than the plan, driven by the conviction that the real direction is now clear. A 1.1% loss. The session drawdown is now $2,900.

Revenge trade two: the trader is certain they have identified the actual move. A 1.4% loss. Total session drawdown: $4,300. The daily limit is breached. The challenge is over.

The original 1.8% loss was survivable. The additional 2.5% from two revenge trades was not. Both revenge trades had explicit rationales. Neither felt impulsive in the moment. The internal experience of both was “I see this.” The outcome was a blown challenge.

That is the architecture: not one large, obviously emotional position, but two or three trades that each felt clean, each had a narrative, and each pushed the account closer to a limit specifically designed to catch this pattern. Whether the challenge uses a static or trailing drawdown limit changes exactly how that cascade plays out — static vs trailing drawdown explained for funded traders covers how each structure creates different pressure at different points in the session. Traders working toward a funded account need to read the daily limit not as a buffer but as the boundary of the session. The evaluation ends when it is hit. There is no session-level recovery mechanism.

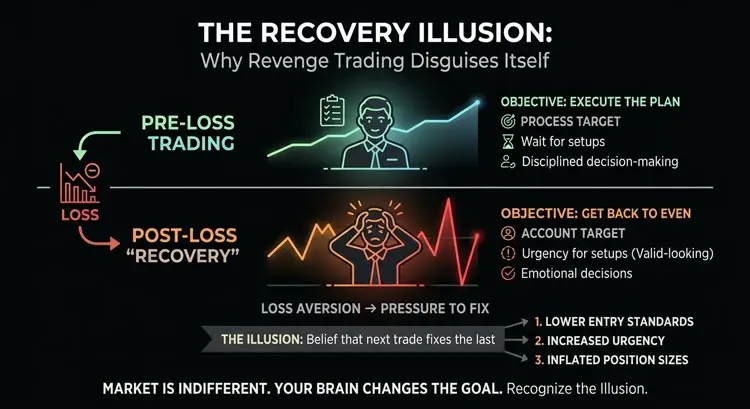

The Recovery Illusion: Why Revenge Trading Disguises Itself as Recovery

There is a specific cognitive error underneath most revenge trading that rarely gets named precisely: the trader’s objective changed without them noticing.

- Before the loss, the objective was: execute the trading plan.

- After the loss, the objective became: get back to even.

These are not the same objective. They produce different decisions, different sizing logic, different patience thresholds for entry conditions. “Get back to even” is an account-relative target with emotional weight attached. “Execute the plan” is a process target that is indifferent to recent results.

The market does not know what your P&L is. There is no such thing as a setup that will “give back” a loss — the loss is crystallised, permanent, and irrelevant to what happens next. Every subsequent trade exists in a market that has no memory of what happened to you this morning. But the brain doesn’t process it that way.

Loss aversion — one of the most replicated findings in behavioural economics — means losses register as roughly twice as impactful as equivalent gains. A 1.5% loss doesn’t just feel like losing 1.5%. It generates a specific pressure to fix something. And the only available mechanism that feels like fixing it is another trade.

This is the recovery illusion: the belief that the next trade exists in relationship to the last one. Under this illusion, the objective quietly shifts from “find a valid setup” to “find a valid-looking setup that can make this back.” The entry standard drops. The urgency rises. The position size inflates in ways that feel reasoned. Revenge trading is what happens when this illusion is operating and the trader has no awareness that it is.

What Actually Interrupts Revenge Trading

The standard advice at this stage — step away from the screen, journal your emotions, take a walk — mostly doesn’t work at the level where revenge trading is genuinely hard to catch. Not because the advice is wrong in principle, but because it requires you to already know you’re in the state. The entire problem is that the state prevents that recognition.

What works are structural rules designed and committed to outside the emotional state, built to trigger automatically without requiring self-awareness in the moment they matter most.

A personal daily stop-loss, set before the session opens. This is separate from the official evaluation limit — a self-imposed ceiling, typically at 40–50% of the official daily limit, that ends your trading day when hit regardless of what you feel in that moment. It must be decided when you are calm, committed in writing or as a hard platform alert, and treated as mechanical. It removes the decision from the emotional state entirely.

A mandatory interval after any losing trade. Before opening the next position, a fixed waiting period must elapse — fifteen minutes, thirty minutes, however long your strategy realistically requires to develop a new setup. This rule requires a clock, not emotional awareness. Most traders who implement a hard interval find that they either skip the revenge trade entirely after waiting, or enter the next trade with a substantially more deliberate process. The urgency state has a half-life. Fifteen to thirty minutes is usually enough to let it decay below threshold.

A pre-trade checklist that cannot be abbreviated. If you cannot complete your full process before entry, you cannot take the trade. This eliminates the theater version of process — running through the checklist in 45 seconds to reach the entry you have already emotionally committed to. Written checklists outperform mental ones because they are significantly harder to truncate without noticing.

Behavioral audit before market analysis after any losing session. The common post-loss review asks why the trades lost. The more diagnostic question is: what were my inter-trade intervals, how did my sizes compare to my baseline, did I stay within my defined strategy, was my pre-trade process completed fully? The behavioral data reveals revenge trading in its early stages. Market analysis usually just confirms the loss was unavoidable — which is often true of the original loss, and irrelevant to the revenge trades that followed it.

These behavioral rules don’t exist in isolation. Practical strategies for passing a prop firm challenge covers the broader consistency and risk management framework that supports them — the psychology layer works best when it sits inside a complete system.

The principle underlying all of these is identical: make the critical decision before the emotional state arrives, so the decision does not have to compete with it in real time. You cannot reliably out-reason a state you don’t know you’re in. You can build a structure that the state cannot override.

For traders working to get a funded account through a prop firm challenge, these aren’t soft psychological habits. They are the operational layer that determines whether a genuine edge survives an evaluation — or gets dismantled by two or three trades that each felt like the right call.

Revenge trading ends more evaluation accounts than poor strategy does. Most traders who fail challenges are not running a broken system — they are running a sound system in an unsound state. The account doesn’t fail because the edge doesn’t work. It fails because one losing session triggered a sequence that the daily limit was built specifically to catch.

The fix isn’t abstract emotional resilience. It’s structural: rules built outside the state, applied mechanically, before the urgency arrives. A prop firm evaluation is a controlled environment with hard limits. Revenge trading is how traders hand it those limits willingly, one justified-feeling trade at a time. For traders still deciding which challenge to pursue, how to get a funded trading account in 2026 covers what to look for before the emotional pressure of a live evaluation begins.

Miles Rowan Keene

As Senior Market Strategist at PropLynq, I write about market structure, trading psychology, and risk-first execution. My focus is on turning complex market behavior into clear, actionable lessons for both developing and experienced traders. I specialize in educational content covering funded account rules, drawdown management, trade planning, and strategy refinement, with the goal of helping traders build consistency through discipline, preparation, and a deeper understanding of how professional trading environments operate.

Weekly Trading Insights

Market analysis and trading tips delivered every Monday. No spam, unsubscribe anytime.

Comments

All comments are reviewed before publication · Text only · No links

No comments yet — be the first.