How to Get a Funded Trading Account in 2026 and Scale Smart

Funded Trading Account remains one of the most attractive paths for new traders in 2026 because it offers access to larger capital without requiring a large personal trading account. In the retail funded-account world, that usually means joining a prop firm, following a defined ruleset, and earning a profit split if you trade consistently within the firm’s risk limits.

That opportunity is real, but it is often misunderstood. A funded account is not simply “free capital.” It is capital attached to an evaluation process, loss limits, payout rules, and performance pressure. Many beginners focus on the advertised account size and overlook the details that determine whether they can keep the account long enough to benefit from it.

The right way to think about funded accounts is not “Which firm has the biggest number?” (Definitely PropLynq !)but “Which funding model fits my strategy, my risk tolerance, and my ability to stay disciplined?” That question matters more than any headline discount or oversized account promise. A trader who chooses the right structure can build consistency, qualify for payouts, and work toward larger capital allocation. A trader who chooses the wrong structure usually discovers it through broken rules, avoidable drawdown, and unnecessary stress.

What funded trading accounts in 2026 means for beginners

For most retail traders, funded account no longer looks like a traditional institutional desk role. It usually means entering a structured funded-account environment where the firm defines the account model, the drawdown rules, the payout structure, and the scaling path. Your job is to show that you can trade responsibly inside that framework.

That changes what success looks like. In prop trading, success is rarely about one huge trade. It is about surviving the evaluation, protecting the funded account, qualifying for withdrawals, and showing enough stability to earn more capital over time. In other words, process matters more than excitement.

This is why the most important part of funded accounts is often the least glamorous part. New traders tend to pay attention to “instant funding,” “high profit split,” or “scale to millions.” Those details matter, but only after you understand the rules underneath them. A high account balance does not help much if the drawdown model is too tight for your strategy. A generous profit split is less valuable if the payout timing, minimum trading-day requirements, or platform restrictions do not fit how you actually trade.

The appeal is still obvious. Funded accounts reduce the need to risk large personal capital. They also create structure, and that structure can improve a trader’s habits. Clear rules force better position sizing, better self-control, and more honest feedback. If you can follow a plan, funded accounts can help you build discipline faster than loosely managed self-funded trading.

The same structure can also expose weak habits very quickly. Traders who chase targets, overleverage, revenge trade, or constantly switch strategy usually struggle in funded environments because the loss limits are not theoretical. A prop firm is effectively asking one question: can you manage risk well enough to deserve more capital? If the answer is yes only when conditions are perfect, the funded trading account model will usually reveal that sooner rather than later.

How to get a funded trading account in 2026

Getting a funded trading account is usually less about finding a shortcut and more about proving that you can operate inside a professional ruleset. The exact path differs by firm, but the logic is usually the same: choose the right model, understand the funded account evaluation process, prepare your own risk plan, pass the challenge or meet the funding criteria, and then protect the account once you have it.

1. Choose the model that fits your trading style

The first decision is not which firm advertises the biggest balance. It is which account structure gives you the best chance of trading your existing setup without forcing bad behavior.

A one-step prop challenge usually appeals to traders who want a quicker route and can handle tighter pressure. A two-step challenge spreads the process over more than one phase, which can suit traders who prefer a slower proof-of-consistency path. Lite-style programs often sit between flexibility and pressure. Instant-funding accounts remove the pre-funding evaluation phase, but they still come with strict loss limits and their own commercial trade-offs.

The key is fit. If your strategy needs patience and controlled execution, a slower evaluation can help you trade more naturally. If you are already consistent and want faster access to capital, instant funding may be worth evaluating. The best choice is the one that lets you follow your real process, not the one that sounds the most exciting in a banner.

2. Learn the evaluation process before you pay

Many beginners make the same mistake: they buy a prop challenge first and study the rules later. That is backwards.

Before paying for any prop account, read the full rule structure and ask a simple question: can I realistically execute my strategy inside these limits without forcing trades? That means checking the profit target, daily loss cap, maximum drawdown, minimum trading days, payout timing, and any restrictions around news trading, holding trades, expert advisors, or platform use.

If you need to trade very differently just to survive the account, the problem is not motivation. The problem is fit. A funded-account model should reward disciplined execution. It should not push you into random aggression just to satisfy a number.

3. Build your risk plan before the funded account challenge starts

Once you understand the funded account rules, build your own plan before the challenge begins. That plan should cover position sizing, maximum risk per trade, maximum number of trades per day, market conditions you will avoid, and what you will do after a losing streak.

This step matters because prop rules are guardrails, not a trading plan. If the firm says you can lose a certain amount in a day, that does not mean you should trade anywhere near that limit. Strong traders usually set tighter personal rules than the firm requires. They think in terms of preserving optionality, not using every inch of allowed drawdown.

A simple framework works well for most beginners in most prop firms:

- define a fixed maximum risk per trade

- define a smaller personal daily stop than the firm’s hard limit

- reduce size after a rough day or a sequence of poor executions

- avoid trading just because you feel pressure to “make progress”

4. Pass, then protect

Passing a funded account challenge is not the finish line. It is the point where a different kind of discipline starts. Once funded, the focus should shift from “How fast can I hit another target?” to “How cleanly can I keep this account, qualify for payouts, and earn larger allocation over time?”

That means using the same risk discipline that got you there. Many traders pass an evaluation, feel relief, then increase size too early because the funded account feels more valuable. That is one of the fastest ways to lose the opportunity they worked for.

Common beginner mistakes in funded trading accounts

Most failures happen for simple reasons:

- risking too much to hit the target quickly

- ignoring payout rules until after passing

- choosing a firm because of discounts instead of rule fit

- changing strategy in the middle of the challenge

- treating one strong week as proof of long-term readiness

A funded account is usually earned through repeatable execution, not dramatic performance. The traders who last are the ones who protect the account first and treat capital allocation as something to deserve, not something to gamble with.

Funded account requirements you should check before buying

The most important proprietary trading firm requirements are usually not the most visible ones on the sales page. What matters most is whether the rules are clear, realistic, and compatible with the way you trade.

Start with drawdown. This is often the single most important rule because it determines how much normal market fluctuation your strategy can survive. Two firms can advertise similar account sizes but feel completely different in practice if one uses a tighter or less forgiving drawdown structure.

Next, compare the relationship between the profit target and the allowed loss. If the target is ambitious relative to the drawdown limit, traders often feel forced to take poor-quality setups just to progress. A funded trading account challenge should still require skill, but it should not quietly reward desperation.

Then check the timing rules. Are there minimum trading days? Is there a time limit to pass? Is there an inactivity rule? Do you have to wait for a particular payout window before withdrawing? These rules can change how you pace the account, and they matter more than many beginners expect.

Operational fit matters too. Look at the platform, the broker setup, whether expert advisors are allowed, whether certain styles are restricted, and whether the firm clearly explains how the environment works. The more visibility you have before purchase, the easier it is to make a rational decision.

A simple checklist helps:

- How is drawdown measured?

- What is the daily loss limit?

- What is the maximum drawdown?

- Are there minimum trading days?

- Is there a time limit?

- When do payouts become available?

- Are there restrictions on your strategy, platform, or tools?

- Is the scaling plan clearly explained?

These requirements are not just policy details. They tell you what type of trader the firm is actually trying to fund. Clear rules usually signal a more professional environment. Vague or hard-to-interpret rules often create problems later, especially for beginners who assume the marketing page tells the whole story.

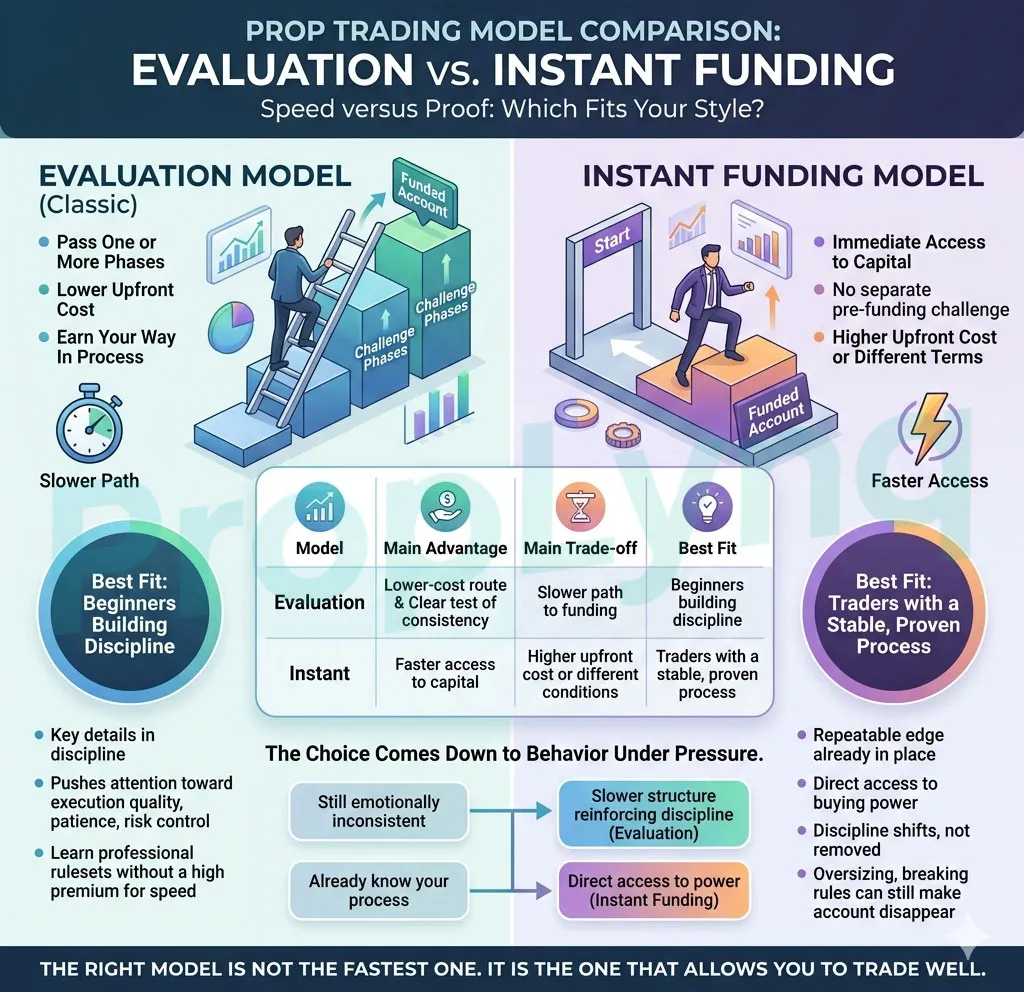

Evaluation vs instant funding: which one fits your style?

One of the biggest decisions in funded account trading is whether to choose a classic evaluation model or go straight to instant funding. The difference is usually framed as speed versus proof.

Evaluation models ask you to pass one or more phases before you receive a funded account. That usually means a lower upfront cost and a more traditional “earn your way in” process. Instant funding gives immediate access to an account without a separate pre-funding challenge, but that speed usually comes with a higher upfront cost or different commercial terms. It does not remove the need for discipline. It simply changes when the screening happens.

Here is the practical difference:

| Model | Main advantage | Main trade-off | Best fit |

|---|---|---|---|

| Evaluation | Lower-cost route and a clear test of consistency | Slower path to funding | Beginners building discipline |

| Instant funding | Faster access to capital | Higher upfront cost or different conditions | Traders with a stable, proven process |

An evaluation model often makes more sense when the main goal is learning how to trade inside a professional ruleset without paying the highest premium for speed. It can also help slow down traders who tend to rush. Because the challenge has to be passed first, it naturally pushes attention toward execution quality, patience, and risk control.

Instant funding can make sense for traders who already have a repeatable edge and want faster access to buying power. The mistake is assuming “instant” means “easy.” It usually removes the qualifying stage, not the consequences of poor trading. If you oversize, break rules, or ignore the drawdown structure, the account can still disappear quickly.

This choice comes down to behavior under pressure. Traders who are still emotionally inconsistent often do better in a slower structure that reinforces discipline. Traders who already know their process may value direct access more. The right model is not the fastest one. It is the one that allows you to trade well.

How to scale without losing the funded account

Scaling is one of the biggest reasons traders enter funded account firms, but it is also one of the easiest places to become unrealistic. A scaling plan is not permission to trade harder. It is a system for increasing capital allocation after you prove that your current level is under control.

That distinction matters because many traders think scaling begins when they get funded. In reality, scaling begins with the habits that make a funded account survivable: stable position sizing, controlled losses, consistent execution, and the ability to stay patient when the market is not offering much.

The first rule of scaling is simple: protect the account before trying to grow it. That means thinking like a risk manager first. If the firm allows a certain level of loss, your personal rules should usually be tighter. The closer you live to the hard limits, the less room you have to recover calmly.

A practical scaling framework looks like this:

- trade small enough that normal losing streaks do not threaten the account

- maintain the same process through ordinary weeks, not only when conditions are ideal

- reduce size when execution quality slips

- increase only after a meaningful run of disciplined performance

- judge progress by stability, not by one strong payout cycle

The psychological side is just as important as the numerical side. During the evaluation phase, traders often fear failing. During scaling, they often fear giving back progress. Both states can produce the same bad behavior: hesitation, impulsive trades, forced setups, or abandoning a plan that was working.

That is why scaling plans should include behavioral rules, not just financial ones. Examples include stopping after a defined loss threshold, lowering size after consecutive red days, journaling emotional state alongside trade execution, and avoiding “celebration risk” after a strong period. Bigger capital amplifies mistakes just as easily as it amplifies gains.

The traders who reach larger allocation are usually not the ones chasing every milestone. They are the ones who make the firm comfortable giving them more room. In funded account, trust is built through repeatability.

How to compare prop firms in 2026 — and where PropLynq fits

When comparing prop firms, beginners often start with discounts, account size, or the boldest promotional message. A better process is to compare five things in order:

- account model

- drawdown structure

- timing rules

- payout mechanics

- scaling logic

That shortlist is simple, but it is usually enough to eliminate poor fits quickly.

Start with the prop firm account model. Does the firm offer one-step, two-step, lite, or instant-funding options? Then examine the risk structure. What are the daily loss and maximum drawdown limits, and do they suit the way you trade? After that, move to timing. Are there minimum trading days or inactivity rules? Is there a deadline to pass? How soon can you request a payout? Finally, check whether the scaling path is clearly explained or buried in vague marketing language.

Rule clarity is one of the strongest trust signals in this category. A firm does not need to offer the biggest numbers to be worth considering. It does need to make the product understandable before purchase. Serious traders care more about transparency than hype because unclear rules are expensive.

Viewed through that lens, PropLynq currently presents a fairly straightforward offer. Its site shows four account paths — Stellar 2-Step, Stellar 1-Step, Stellar Lite, and Instant Funding — along with published model comparisons. The broader site positioning includes challenge-based allocation up to $300K, scaling up to $4M, and profit split language up to 95%, alongside a simulated-environment disclosure.

Its live pages also publish several details beginners usually need in order to compare firms properly: no time limit on the main challenge models, instant setup language, read-only monitoring, a visible payouts page, and a defined scaling framework. The site also highlights broker flexibility through an approved-broker structure rather than a one-broker-only approach.

That does not mean a trader should sign up on branding of a prop trading firm alone. The more sensible next step is to compare the available account models, decide which structure fits your trading style, and then read the payout conditions carefully before making a purchase. For PropLynq, that naturally points to the Trading Accounts page first and the Payouts page second.

The broader lesson is useful beyond any single firm. The best prop firms for professional traders are rarely the ones with the loudest marketing. They are the ones that make it easy to understand the rules, evaluate the payout structure, and judge the scaling path in advance. Beginners who borrow that professional screening mindset usually make much better decisions.

FAQ

Is funded trading account good for beginners?

It can be, provided the beginner wants structure and is willing to trade inside strict rules. It is a poor fit for traders looking for a quick win or a way to avoid discipline.

How hard is it to get a funded trading account?

Usually harder than the marketing makes it look. The difficulty is less about opening the account and more about hitting the target without breaking loss rules.

What are the most important prop firm requirements?

Drawdown structure, daily loss limits, timing rules, payout conditions, and any restrictions on trading style or tools.

Is instant funding better than an evaluation?

Not automatically. It is faster, but speed does not remove the need for discipline. For many newer traders, an evaluation model is the more useful training ground.

What should I check before joining a prop firm?

Check the model, the drawdown rules, the payout structure, the timing rules, and whether the firm explains everything clearly enough to evaluate before purchase.

Conclusion

Funded trading account can be a strong route into funded trading, but only when it is treated as a decision about fit rather than a shortcut to larger capital. Traders who last are usually the ones who choose a model that matches their process, study the rules before paying, and build their scaling plan around preservation rather than speed.

For readers comparing options, the most practical next step is to review account structure and payout rules side by side before committing. On PropLynq.com , that means starting with the Trading Accounts page, validating the withdrawal details on the Payouts page, and using the homepage for the broader overview.

Miles Rowan Keene

As Senior Market Strategist at PropLynq, I write about market structure, trading psychology, and risk-first execution. My focus is on turning complex market behavior into clear, actionable lessons for both developing and experienced traders. I specialize in educational content covering funded account rules, drawdown management, trade planning, and strategy refinement, with the goal of helping traders build consistency through discipline, preparation, and a deeper understanding of how professional trading environments operate.

Weekly Trading Insights

Market analysis and trading tips delivered every Monday. No spam, unsubscribe anytime.

Comments

All comments are reviewed before publication · Text only · No links

No comments yet — be the first.