Forex Arbitrage – How Traders Exploit Price Differences Across Markets

Forex markets process trillions of dollars in volume every day, but they do not always price the same currency identically across every venue, broker, or currency pair combination. When a gap appears — even briefly — some traders move to capture it. That practice is forex arbitrage, and understanding it separates traders who genuinely know how currency pricing works from those who only think they do.

This guide explains what forex arbitrage is, how the main types work mechanically, where the real risks sit, and which traders are actually positioned to use it. No theoretical hand-waving — just a clear look with proplynq point of view at how arbitrage functions in modern forex markets.

What Is Forex Arbitrage?

Forex arbitrage is the simultaneous purchase and sale of a currency — or a sequence of currencies — to profit from a temporary price discrepancy between markets, brokers, or currency pair combinations. The defining feature of a true arbitrage trade is that it carries no directional market exposure. You are not betting on a currency moving up or down. You are locking in a difference that already exists in current pricing.

In an ideal market, identical assets price identically everywhere. In practice, forex pricing is assembled from thousands of liquidity providers across fragmented venues. Momentary inconsistencies appear constantly — the question is whether they are large enough and persistent enough to trade profitably after all costs.

Forex arbitrage has not disappeared in the algorithmic era. It has compressed. The windows are smaller and the competition is faster, but the mechanism is unchanged.

How Forex Arbitrage Works

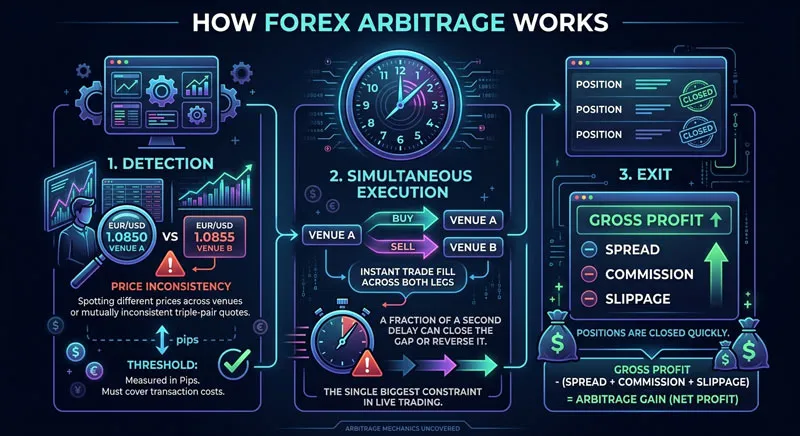

The core logic is simple: detect a price inconsistency, execute offsetting trades simultaneously before it closes, and collect the difference. Execution is where it gets complicated.

The standard sequence for most forex arbitrage strategies runs like this:

- Detection. A system or trader identifies that the same currency pair is priced differently across two venues, or that three currency pair quotes are mutually inconsistent. The gap has to exceed a minimum threshold — typically measured in pips — before it covers transaction costs.

- Simultaneous execution. Both legs of the trade must be filled at essentially the same moment. A delay of even a fraction of a second can close the gap or reverse it entirely. This is the single biggest constraint in live arbitrage trading.

- Exit. Once both legs are filled, the position is closed. The net result — gross profit minus spread, commission, and slippage — is the arbitrage gain.

The brutal reality of modern forex arbitrage is that most detectable gaps last milliseconds. Retail traders using standard platforms are at a structural disadvantage against institutional desks running co-located servers and direct market access. That does not make arbitrage impossible at the retail level, but it does shape which types are viable and which are not.

Transaction costs are the other critical factor. Spreads, commissions, and slippage all erode the margin. If the price gap is 1.5 pips but your round-trip cost is 1.8 pips, there is no trade.

Types of Forex Arbitrage

Forex arbitrage is not a single strategy. It covers a family of approaches that share the same foundational logic but differ significantly in mechanism, speed requirement, and practical accessibility.

| Type | Mechanism | Speed Required | Capital Intensity | Retail Viability |

|---|---|---|---|---|

| Spot Arbitrage | Same pair, different brokers | Very high | Medium | Low |

| Triangular Arbitrage | Three pairs, one venue | High | Medium | Moderate |

| Statistical Arbitrage | Correlation-based mean reversion | Medium | Medium–High | Moderate–High |

| Latency Arbitrage | Quote feed speed differences | Extremely high | High | Very low |

| Interest Rate Arbitrage | Swap and carry differentials | Low | High | Moderate |

Spot Arbitrage

Spot arbitrage exploits a pricing difference for the same currency pair across two different brokers at the same moment. It is the most intuitive form of forex arbitrage and the most aggressively policed. Most retail brokers explicitly prohibit it in their terms of service, and accounts identified as systematically engaging in it risk having trades cancelled or profits reversed.

Triangular Arbitrage

Triangular arbitrage operates within a single venue. If EUR/USD, USD/JPY, and EUR/JPY are not perfectly consistent with each other at a given moment, a trader can convert through all three pairs — EUR to USD, USD to JPY, JPY back to EUR — and end up with more than they started. The opportunity arises from momentary inconsistency in how the three pairs are quoted relative to each other.

Statistical Arbitrage

Statistical arbitrage takes a different approach. Rather than exploiting an instant price gap, it identifies when two historically correlated currency pairs have diverged beyond their normal range and positions for mean reversion. This form of forex arbitrage is slower, more analytical, and more tolerant of short-term adverse movement — making it the most accessible type for sophisticated retail and semi-professional traders who have the quantitative tools to model the relationships.

Latency Arbitrage

Latency arbitrage exploits the time delay between when a price update occurs at one data feed and when it appears at another. Faster participants can effectively trade on the slower feed’s stale price. Without co-location infrastructure and low-latency direct market access, this approach is not realistic for retail participants. It is also the type most likely to trigger broker or platform restrictions.

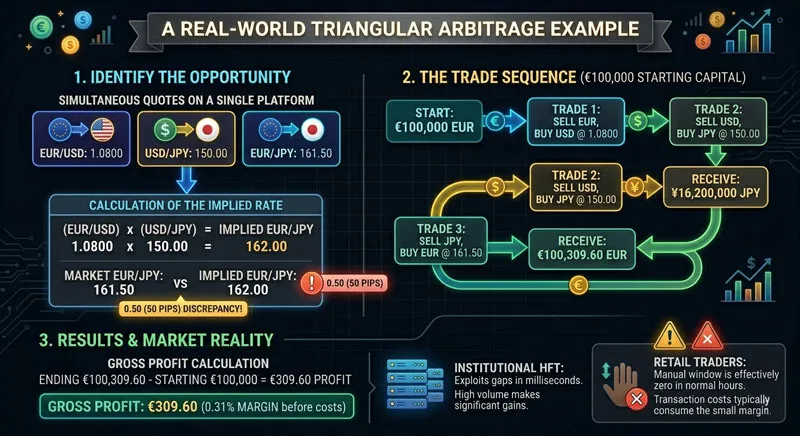

A Real-World Triangular Arbitrage Example

Triangular arbitrage is the most instructive form to walk through step by step because it involves no external brokers and the maths are transparent.

Assume the following quotes are simultaneously available on a single platform:

- EUR/USD: 1.0800

- USD/JPY: 150.00

- EUR/JPY: 161.50

The implied EUR/JPY rate — derived from multiplying EUR/USD by USD/JPY — should be:

1.0800 × 150.00 = 162.00

The market is quoting EUR/JPY at 161.50, which is 50 pips below the implied cross rate. That inconsistency is the opportunity.

Starting with €100,000, the trade sequence runs as follows:

- Sell EUR, buy USD at 1.0800 → receive $108,000

- Sell USD, buy JPY at 150.00 → receive ¥16,200,000

- Sell JPY, buy EUR at 161.50 → receive €100,309.60

Gross profit: approximately €309.60 on €100,000 deployed — a margin of 0.31% before transaction costs. At institutional scale with rapid cycle times across hundreds of iterations, this compounds into meaningful figures. For a single manual retail trade, costs typically consume the entire margin before anything is booked.

In live markets, this gap would close in milliseconds as automated systems detect and trade it away. The window for executing all three legs cleanly by hand is effectively zero in liquid pairs during normal market hours.

Risks and Limitations of Forex Arbitrage

The phrase “risk-free profit” appears often in descriptions of arbitrage. It is accurate only when execution is theoretically perfect. In live forex markets, several factors convert apparent arbitrage gains into losses.

Execution Risk

If one leg of a forex arbitrage trade fills and the second does not — or fills at a meaningfully different price — you are left holding a directional exposure you did not intend. This is called leg-in risk and it is the most common way arbitrage strategies produce unintended losses at the retail level. The faster the strategy, the higher the probability that market conditions shift between the first and second fill.

Transaction Costs

Every forex arbitrage trade incurs spread, commission, and potential slippage on both sides. The all-in round-trip cost must be comfortably below the detected price gap for the trade to be profitable. In highly liquid major pairs, gaps this wide are rare and short-lived. In less liquid pairs, gaps may appear more frequently but spreads are wider — the economics rarely improve.

Broker and Platform Restrictions

Many retail forex brokers explicitly prohibit certain forms of arbitrage in their user agreements — particularly latency arbitrage and two-broker spot arbitrage — on the grounds that these strategies exploit platform infrastructure rather than genuine market price discovery. Accounts identified as using these approaches may face trade cancellations, profit reversals, or account termination. Verifying your trading agreement before deploying any arbitrage strategy is not optional.

Infrastructure Gap

The forex arbitrage opportunities that remain in modern markets after institutional compression typically require low-latency data feeds, fast execution infrastructure, and algorithmic systems running without human delay in the loop. Manual execution is structurally too slow for spot and latency arbitrage in today’s market. Traders without this infrastructure are not competing — they are arriving after the trade is already gone.

Window Compression Over Time

Arbitrage opportunities are self-eliminating. Every participant who detects and trades a price gap helps close it faster. The result is that the most obvious and accessible forex arbitrage windows have been compressed to near-zero in liquid pairs. The remaining opportunities tend to be in less efficient venues, less liquid instruments, or more structurally complex multi-leg configurations that require substantial analytical and technical investment to reach.

Is Forex Arbitrage Right for Your Trading Style?

Forex arbitrage is not a strategy for every trader, and the barriers to entry are often higher than initial research suggests. The type of arbitrage that suits you — if any — depends heavily on your infrastructure, capital base, quantitative skill, and trading context.

Arbitrage May Suit You If

- You have access to multiple liquidity venues or independent data feeds with reliable low-latency connectivity

- You can implement algorithmic or semi-algorithmic execution without manual delay in the process

- Your capital base makes thin per-trade margins worth deploying at meaningful size

- You are focused on statistical arbitrage and have a disciplined quantitative framework for modelling currency pair correlations

- You have confirmed that your broker or trading firm permits the specific type of arbitrage you are planning — in writing, not by assumption

Arbitrage Probably Does Not Suit You If

- You are executing manually on a standard retail platform with no algorithmic support

- Your account size makes the per-trade margins too small to survive the inevitable cost drag

- You have not reviewed whether arbitrage activity is permitted under your trading agreement

- You are looking for a reliable, repeatable edge that does not depend on infrastructure advantages you do not have

Statistical arbitrage remains the most accessible form for serious retail traders because it does not demand millisecond execution. It rewards analytical rigour over raw technology. But it still requires robust backtesting, a clear framework for modelling pair relationships, and consistent position management — the entry bar is analytical rather than infrastructural, but it is still real.

Forex Arbitrage and Prop Firm Evaluation Rules

One dimension of forex arbitrage that traders frequently overlook is how prop firm rules interact with specific arbitrage strategies. Getting this wrong during a funded evaluation is an expensive mistake.

Most prop firms draw a clear distinction between strategies that exploit genuine market price movements and strategies that exploit platform infrastructure or pricing feed inefficiencies. Latency arbitrage and two-broker spot arbitrage typically fall into the second category and are prohibited under standard funded account agreements — even when the trades are technically profitable.

Statistical arbitrage and pairs trading strategies, by contrast, are more likely to be viewed as legitimate quantitative approaches, provided they operate within the firm’s drawdown limits, position sizing rules, and holding period constraints.

At PropLynq, the evaluation framework is designed around real market risk. Strategies that are genuinely market-facing — generating edge from price analysis rather than from feed-speed advantages — have a clear path through the process. Before deploying any arbitrage-adjacent approach on a funded account, the right step is to read the firm’s evaluation rules carefully and, if in doubt, ask directly before the evaluation begins rather than after a trade has been flagged.

Traders preparing for a PropLynq evaluation can review the full set of permitted strategy types and risk parameters in the evaluation documentation to confirm whether their approach qualifies.

Final Thoughts on Forex Arbitrage

Forex arbitrage is real, active, and structurally important to how markets maintain pricing consistency — but it is not the accessible edge it is sometimes marketed as. The fastest opportunities require institutional infrastructure. The most accessible opportunities require quantitative skill. And all of them require a thorough understanding of the rules governing the venue where you trade.

For traders who approach forex arbitrage seriously — with realistic expectations, a strategy matched to their actual capabilities, and full clarity on what their broker or prop firm permits — the discipline is genuinely valuable. Even traders who never execute a pure arbitrage trade benefit from understanding the concept: it sharpens how you read pricing, think about spreads, and evaluate whether a market opportunity is real or illusory.

Miles Rowan Keene

As Senior Market Strategist at PropLynq, I write about market structure, trading psychology, and risk-first execution. My focus is on turning complex market behavior into clear, actionable lessons for both developing and experienced traders. I specialize in educational content covering funded account rules, drawdown management, trade planning, and strategy refinement, with the goal of helping traders build consistency through discipline, preparation, and a deeper understanding of how professional trading environments operate.

Weekly Trading Insights

Market analysis and trading tips delivered every Monday. No spam, unsubscribe anytime.

Comments

All comments are reviewed before publication · Text only · No links

No comments yet — be the first.